|

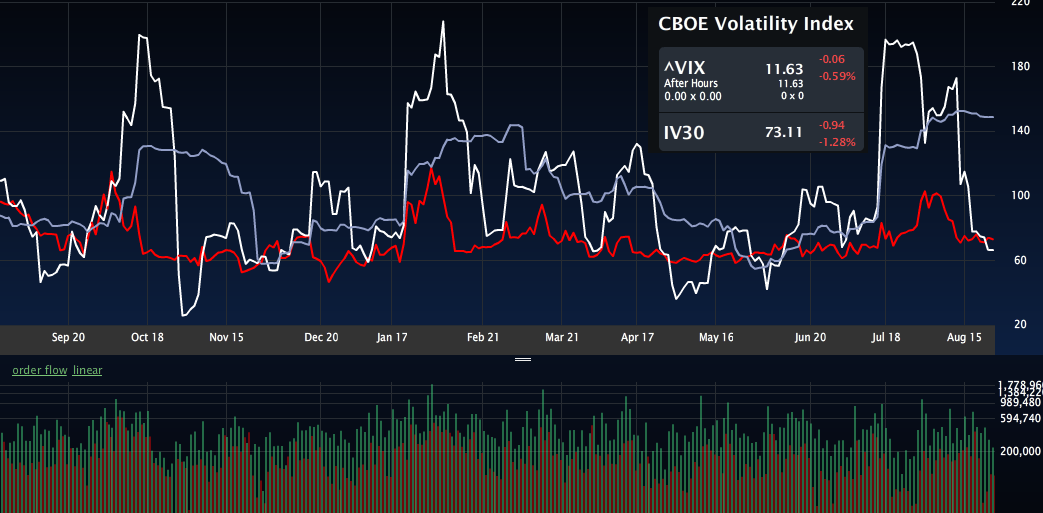

| The VIX as of today's close. HV10: White; HV30: Gray; IV30: Red |

The S&P500 itself has been flirting above and below the 2000 milestone for the past two days, showing uncertainty of whether this millennial mark can maintain despite the trimming of the Fed's balance sheet and the looming possibility of interest-rate risk.

|

| $SPY: HV10: White; HV30: Gray; IV30: Red |

Below is the options skew for $SPY:

Based on options sales in the $SPY, one trader is betting on S&P upside to the 2002.5 level with the purchase of 5200 call options on the index. This level acted as strong resistance in this afternoon's trading.

|

| Largest sales in the $SPY today |

On the flip-side, a bearish ante was upped today with the sale of a 10,000 put option spread for the 19300 and 19900 levels. This trader is betting on downside retracement to the levels seen earlier this month before the magnificent 65-handle, 10 trading day rally:

From either perspective, bet on increased chop in the days ahead.

|

| Largest VIX sales for Aug. 26, 2014 |

A 15000-lot 18/23 call spread was opened today for the Oct. $VIX expiry. For those of you betting on increased volatility as we head into the fall, the current 30-day implied volatility of the VIX sits near 70, which indicates that the IV30 of the VIX has only been lower 33% of the time.

Good luck tomorrow.

0 comments:

Post a Comment