| |

| The landscape of fear |

Today's market is pricing in yesterday's fear. Of course, today is not yesterday, but Wall Street utilizes the approximate past to price the proximate future:

|

| The landscape of tail risk |

The skew of $VIX option sales prices-in 2001, 2008, and everything in between. In other words, the contango between VIX spot and VIX futures reflects an elevated premium that will yield minimum profits to a VIX call buyer should a "black swan" event of similar magnitude to 2008 occur during the life of the contract.

VIX options have been available since 2006 and one can conclude that the markets have had sufficient time to discover the price of risk and volatility in this instrument.

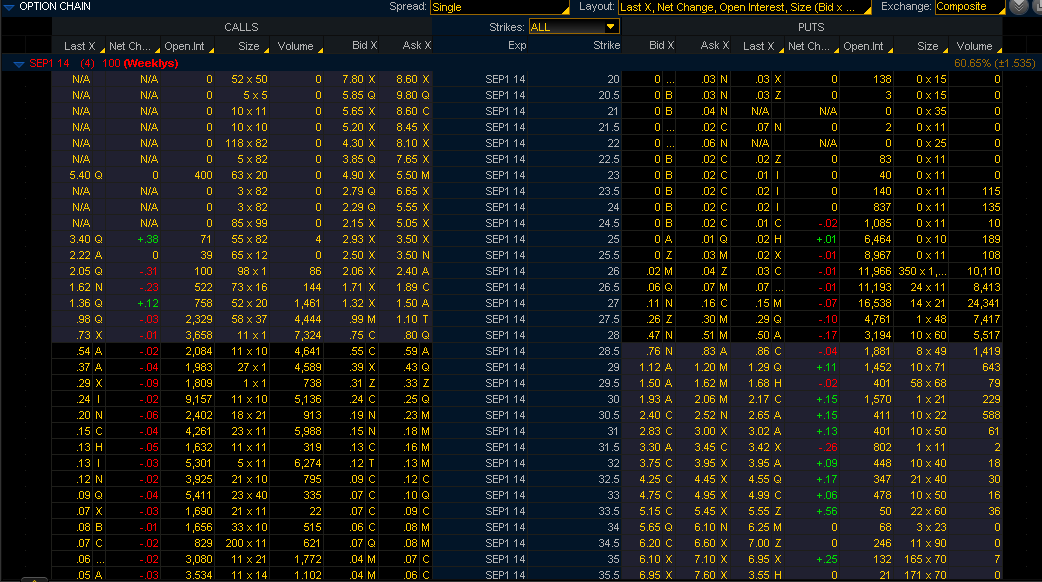

The VXX allows one to go long or short front-end contracts in VIX futures. The advantage of this instrument can be seen in the fact that its prices are not necessarily a reflection of the implied movement in the S&P, but rather seems to be normalized to the volatility extremes of 2008-9:

The exponential downward movement (minus the minor volatility flashes of 2010 and 2011) reflects the new paradigm of risk since QE. Looking at the magnitude of the movement in this instrument reflects wider potential variance in the instrument. However, the VXX itself has been limited to sub-100 levels for quite some time. However, given that, a look at the options grid shows that trading this instrument can prove to be more profitable than the highly subdued VIX:

The instrument can be traded in half-integer intervals, allowing exposure to smaller movements in near-term volatility. You should also notice that the premiums of calls vs. puts do not diverge as heavily as the VIX since one's fundamental position is in short-term volatility. Having monitored this instrument myself, the VXX is highly vega sensitive. Therefore, owning this instrument also carries the responsibility of being closely monitored and also carefully timed entrances and exits.

Taking a look at the options skew above for VXX shows a less steep implied volatility compared to the VIX.

Having flirted with the 2000 level in the S&P500 for the past several days, I talked about the potential for increased market volatility based on options and futures sales last week. Having said that, please remember that volatility still has room to go down, at least until rates continue to stay low.

Good luck tomorrow.

0 comments:

Post a Comment