The S&P500 closed just south of 1978 today after trading within a 15-point range. We saw a strong late-day 10-point rally which nearly drove the index positive for the day.

|

| Supports and resistance in $SPX |

Where are we headed from here? Let's take a look at some historical and forward looking data.

September marks the end of the 3rd quarter. Taking a look back at the past few years, we've seen selling in the S&P that coincides with the end of the summer. The chart below shows the transition from summer into fall in 2013:

|

| 2013 Q2/Q3 transition in $SPX |

Looking at the data from 2013, we saw a mid-September all-time high in the S&P followed by a sell-off right into the end of the month. October then saw brand new highs. We've seen similar activity thus far in the S&P this year: all-time highs in mid-September followed by an end of the month sell-off. Now let's look further back into 2012:

|

| 2012 Q2/Q3 transition in $SPX |

In 2012, we also saw mid-September all-time highs in the index followed by a sell-off. An attempt at a new all-time high started several days before October but stopped just shy of it.

2011 tells a different story in the S&P500:

|

| 2011 Q2/Q3 transition in the $SPX |

Going into fall 2011, the index saw nearly a 250-point drop from July to August which had traders and money managers a little more reluctant to attempt all-time highs in September. We did however see a decent sized rally in mid-September followed by a sell-off that coincided with the end of the month.

In 2010, the S&P saw a nearly uninterrupted rally right into Q4 with only some minor pullbacks at the end of September:

|

| 2010 Q2/Q3 transition in the $SPX |

What can we take away from this data? First of all, this sell-off we are experiencing in the US indexes seems to be typical of market behavior during this time of year. Of course, the magnitude of selling depends highly on the environment. In 2010, we were still in the early stages of quantitative easing. So looking back at the data from that year, we can perhaps see why the markets saw a rally straight through October. As the years progress, we've seen a trend of increased selling in the summer to fall transitional period that intuitively makes sense as the Fed's money policy begins to tighten.

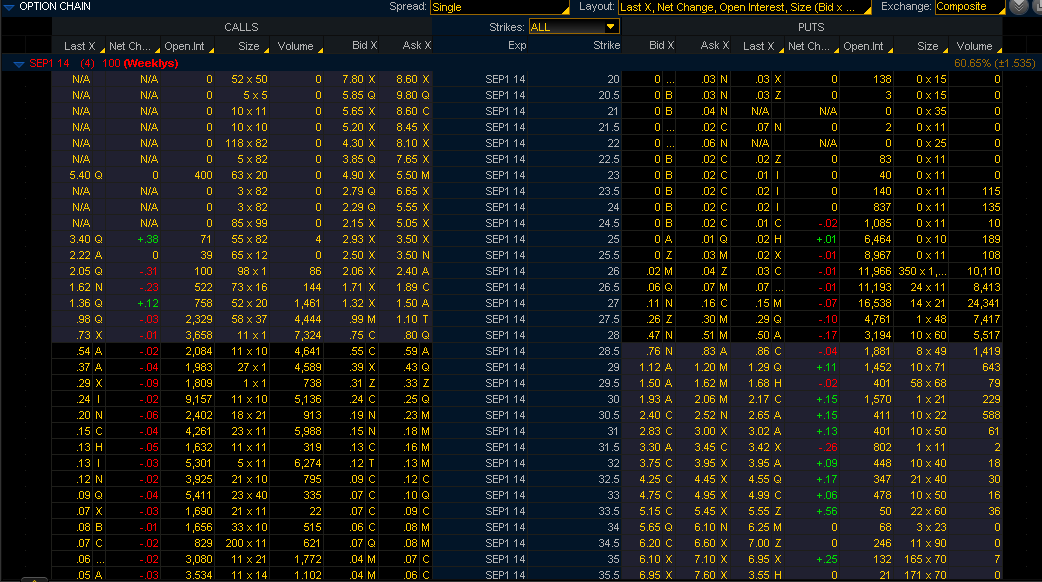

So what can we expect for this year's September to October transition? Let's take a look at the option skew in $SPY based on today's sales:

|

| The quarterly expiration for $SPY |

By the end of today, traders seem to have developed some optimism in the S&P. We see a well defined parabolic skew in option sales which indicates equally bullish and bearish bets on the index by the end of tomorrow's trading day (and the end of Q3).

In the past weeks when the S&P was entrenched in the 2000 level tango, I showed you option skews in the index which showed

only pessimism in the future direction of US markets. The following $SPY skew is from earlier this month (Sept. 9):

|

| $SPY option skew from September 9 |

The above skew is a nice example of market pessimism. A few days before September 9th, we hit a new all-time high in the S&P of 2011.00 which had the markets a little frightened. We did see a slight pullback in the days following only to see another all-time high of 2020.

So taking a look back at today's option skew in $SPY, we can extrapolate that traders are a little more optimistic especially in light of the much needed pull back from those all-time highs.

Finally, let's take a look at what the $VIX has to say about all of this:

|

| Volume bars - Green: Calls sold; Red: Puts sold |

The VIX rose a whopping 7.6% today with an even greater increase in the implied volatility. The volatility of volatility rests just south of 100, which historically speaking, represents a higher value than 60% of the time in the past 52-weeks. Despite the bullish bets made on the markets today, the VIX implies a lot of anxiety still lurking beneath the surface.

Please exercise caution when trading within an environment of elevated volatility, and as always, good luck tomorrow.

{kind=link}